When Industry Margins Tighten: What the Healthcare Crunch Means for Your Creator Capital

What changed

Healthcare providers are facing a sustained financial squeeze that could signal broader shifts in lending markets. According to data from CTI Leadership, industry EBITDA as a percentage of national health expenditures has dropped significantly, falling from 11.2% in 2019 to 8.9% in 2024 CTI Leadership. This downward trend is being exacerbated by policy shifts, including projected Medicaid rate reductions and a surge in uncompensated care costs, which the California State Government projects will increase by $1 billion annually by 2030 California State Government.

How it works

The mechanism is straightforward: when sectors like healthcare face margin compression, capital providers—banks and private lenders—become more defensive. Both the California state analysis and CTI Leadership data confirm a unified picture of financial fragility in the health sector California State Government, CTI Leadership. While these sources differ in their specific focus—one on state-level policy impact and the other on national EBITDA percentages—they agree that the fundamental stability of these businesses is eroding. When major sectors suffer from lower operating margins, lenders often rebalance their portfolios, meaning capital that might have been easily deployed to small businesses (including creative studios) may be tied up in risk mitigation or redirected toward more stable, higher-collateral opportunities.

Who it hits

The immediate victims are healthcare clinics and providers, but the ripple effects touch any small business owner reliant on external credit. Because EBITDA margins are a primary metric lenders use to determine creditworthiness and risk premiums, a sector-wide decline often leads to stricter "tightened" underwriting criteria across the board. If the market perceives that businesses generally have less "cushion" to absorb shocks, financing becomes more expensive and harder to access.

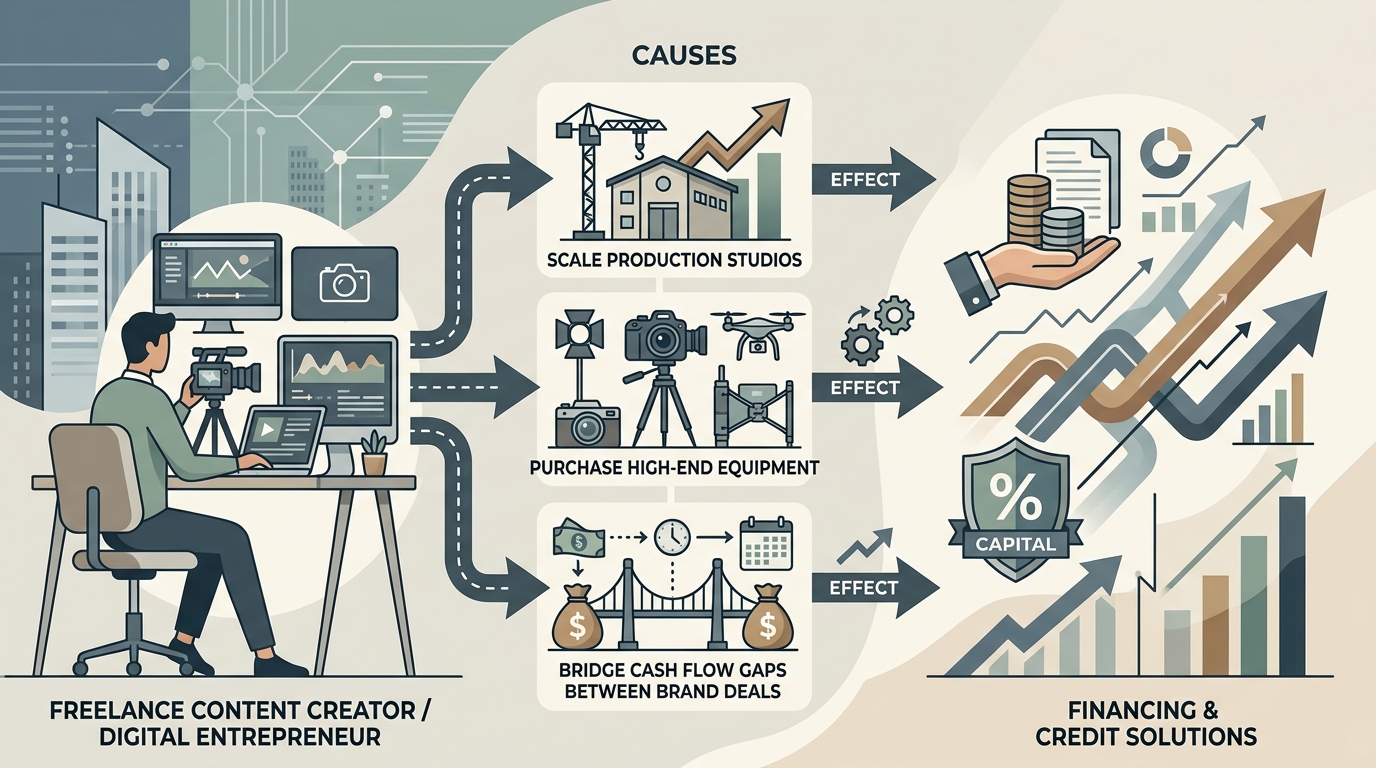

Why this matters for Full-time freelance content creators and digital entrepreneurs seeking capital to scale their production studios, purchase high-end equipment, or bridge cash flow gaps between brand deals.

For a digital entrepreneur, the connection to healthcare policy might seem remote, but the implications for your production budget are real. When lenders observe systemic margin pressure in major industries, they often tighten their "risk appetite" for all small business loans. This means that if you are seeking a term loan for a new $50,000 camera package or a line of credit to smooth out the 60-day lag between invoice and payment from brand partners, you may encounter higher documentation requirements and stricter cash-flow verification.

In periods of macro-economic uncertainty, "easy money" dries up. You should anticipate that lenders will scrutinize your EBITDA (or net profit) more closely than they did in 2021 or 2022. Expect fewer "stated income" loan products and more requests for detailed P&Ls or three-year business plans. If you are planning a capital expenditure for late 2026, it is prudent to secure your financing now while your credit profile is strong, rather than waiting until macroeconomic trends force lenders to raise their hurdle rates.

Bottom line

Systemic margin compression in major sectors forces lenders to tighten underwriting standards across the board, making capital harder to secure for small businesses. Protect your production studio by locking in credit lines now rather than waiting for future market corrections.

Check your eligibility for current equipment financing options today.

Disclosures

This content is for educational purposes only and is not financial advice. thecreator.market may receive compensation from partner lenders, which may influence which products are featured. Rates, terms, and availability vary by lender and applicant qualifications.

What business owners say

4.9-

This company was lightning fast and the experience was amazing. Thank you, Dan — you're a real pro!

-

Good service Joseph Krajewski is the best agent ever. He provided excellent service. I strongly recommend working with him if you have the opportunity.

-

They gave me a chance when nobody else would. I'm very satisfied.

Frequently asked questions

Why does a decline in healthcare margins matter for content creators?

Capital markets are interconnected. When specific sectors experience sustained margin compression and increased risk, lenders often tighten their broader risk appetite, which can affect credit availability and pricing for all small business borrowers.

What is 'uncompensated care' and why is it a budget threat?

Uncompensated care refers to services provided where no payment is received, either from the patient or insurance. As costs for this rise, it erodes the operating profit (EBITDA) of clinics, forcing lenders to reassess the risk profile of lending to that sector.

Will my equipment financing rates increase because of this?

Not directly. However, when major industries face sustained margin drops, lenders often shift toward more conservative underwriting standards. You may find it harder to secure unsecured lines of credit if macro-economic volatility increases across sectors.

- Glendale Creator Financing and Credit Solutions for Digital Content Creators (19/06/2026)

- Financing and Credit for Digital Content Creators in Amarillo, Texas (19/06/2026)

- Financing and Credit Solutions for Professional Digital Content Creators in Yonkers, New York (19/06/2026)

- Financing and credit solutions for professional digital content creators in Frisco, Texas (19/06/2026)

- Financing and Credit Solutions for Professional Digital Content Creators in Salt Lake City, Utah (18/06/2026)

- Financing and Credit Solutions for Professional Digital Content Creators in Huntsville, Alabama (18/06/2026)

- Grand Rapids Financing and Credit Solutions for Professional Digital Content Creators (18/06/2026)

- Financing and Credit Solutions for Professional Digital Content Creators in Rochester, New York (18/06/2026)